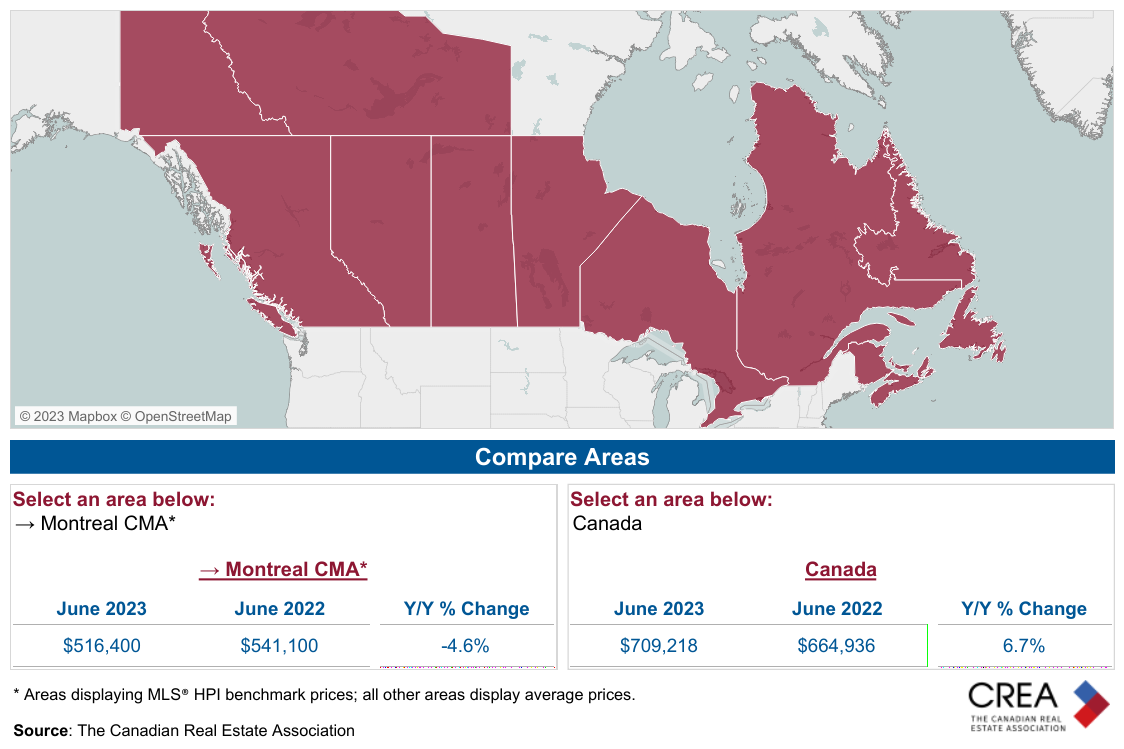

MLS® Home Price Index explained

|

The MLS® HPI is a measure of real estate prices that provides a clearer picture of market trends over traditional tools such as mean or median average prices.

A mean average is the average price obtained by dividing the total dollar volume of sales by the number of sales. To get a median price, all of the sales prices are arrayed in numeric order. In the case of an even number of sales, the median is the highest price in the lower half of the group. If there is an odd number of sales, the midpoint sale is taken as the median. The MLS® HPI concept is modelled after the Consumer Price Index, which measures the rate of price change for a basket of goods and services. A basket is the combination of goods and services that Canadians buy most such as food, clothing, transportation, etc. Instead of measuring goods and services, the MLS® HPI measures the rate at which housing prices change over time taking into account the type of homes sold. |

|

The problem with averages before the original HPI was introduced in 1996, REALTORS® and the public relied on monthly average pricing statistics to understand trends in housing prices.

Averages, however, can be very misleading since the quantity and quality of the properties sold in any given area change over time for any number of reasons. As a result, average prices can fluctuate dramatically, making the housing market appear unstable. To demonstrate this point, let’s look a couple of examples of how average prices are affected by various changes in sales patterns |

|

Example 1: How mean averages are affected by price changes Year 1 ($)Year 2 ($) 1. 139,0001. 139,000 2. 145,0002. 145,000 3. 230,0003. 230,000 4. 265,0004. 265,000 5. 290,000 median average5. 290,000 median average 6. 320,0006. 320,000 7. 365,0007. 365,000 8. 425,0008. *545,000 9. 480,0009. *580,000 Total $2,659,000 ÷ 9 sales = $295,444, which is the mean averageTotal $2,879,000 ÷ 9 sales = $319,888, which is the mean average *price change from Year 1 In this example, the mean average increased by 7.7 percent while the median average stayed the same. This shows that price changes at either end of the price scale affect the mean average, but can leave the median average virtually unchanged. |

Example 2: How median averages are affected by price changes Year 1 ($)Year 2 ($) 1. 139,0001. 139,000 2. 145,0002. 145,000 3. 230,0003. 230,000 4. 265,0004. *290,000 5. 290,000 median average5. *320,000 median average 6. 320,0006. *335,000 7. 365,0007. *395,000 8. 425,0008. *400,000 9. 480,0009. *405,000 Total$2,659,000 ÷ 9 sales = $295,444, which is the mean averageTotal$2,659,000 ÷ 9 sales = $295,444,which is the mean average *price change from Year 1 In this example, the mean average stayed the same while the median average increased by 9.4 percent. This shows that price changes in the mid-range section of the price scale affect the median average, but can leave the mean average virtually unchanged. Neither of these price measurements take into account the changes in buying pattern — In year one luxury homes in the region are popular; the following year more modestly priced homes are popular. Both methods of price tracking can have the effect of overestimating the market price that home buyers are actually paying for their homes. |

Defining the typical homeThe MLS® HPI is a more stable price indicator than average prices, because it tracks changes of "middle-of-the-range" or "typical" homes and excludes the extreme high-end and low-end properties.

Typical homes are defined by the various quantitative property attributes (e.g. above ground living area in square feet) and qualitative housing features (e.g. proximity to shopping, schools, transportation, hospitals etc.) toward the home price of properties sold in Greater Vancouver communities.

These features together become the "benchmark" house, townhouse or apartment in a given area. A benchmark property is designed to represent a typical residential property in a particular MLS® HPI housing market, such as Richmond or North Vancouver.

For example, perhaps the basket of features for a typical home in a given community includes a 10-year-old, 3-bedroom house without a panoramic or ocean view on a 7,200 sq. ft. lot, with 8 rooms, 2 bathrooms, a fireplace, a 1-car garage and is close to schools. A benchmark price for this home can be created from the individual dollar values given to each of the above features.

The breakdown of each month’s real estate sales in a given area are estimates of current prices paid for bedrooms, bathrooms, fireplaces, etc. Prices for these qualitative and quantitative features are then applied to the typical house model and an index price is estimated for that month. This type of pricing model involves estimating the price of a property’s features rather than the property itself.

Note: The MLS® HPI offers only a benchmark in which to track price trends and consumers should be careful not to misinterpret index figures as actual prices. Benchmark properties are considered average properties in a given community and do not reflect any one particular property.

Typical homes are defined by the various quantitative property attributes (e.g. above ground living area in square feet) and qualitative housing features (e.g. proximity to shopping, schools, transportation, hospitals etc.) toward the home price of properties sold in Greater Vancouver communities.

These features together become the "benchmark" house, townhouse or apartment in a given area. A benchmark property is designed to represent a typical residential property in a particular MLS® HPI housing market, such as Richmond or North Vancouver.

For example, perhaps the basket of features for a typical home in a given community includes a 10-year-old, 3-bedroom house without a panoramic or ocean view on a 7,200 sq. ft. lot, with 8 rooms, 2 bathrooms, a fireplace, a 1-car garage and is close to schools. A benchmark price for this home can be created from the individual dollar values given to each of the above features.

The breakdown of each month’s real estate sales in a given area are estimates of current prices paid for bedrooms, bathrooms, fireplaces, etc. Prices for these qualitative and quantitative features are then applied to the typical house model and an index price is estimated for that month. This type of pricing model involves estimating the price of a property’s features rather than the property itself.

Note: The MLS® HPI offers only a benchmark in which to track price trends and consumers should be careful not to misinterpret index figures as actual prices. Benchmark properties are considered average properties in a given community and do not reflect any one particular property.